When you’re busy working, earning, and enjoying life with your family, it’s easy to put your pension on the back burner. After all, retirement seems like a far away dot on the horizon, so there’s nothing to worry about for now.

But the truth is, the cost of retirement is going up. The Pensions and Lifetime Savings Association (PLSA) says that a “moderate” retirement now has an annual cost of £31,300 for a single person, or £43,100 for a couple. A “comfortable” retirement could cost a single person £43,100 a year, or £59,000 a year for you and your spouse or partner.

These costs are likely to continue rising in the coming years. With this in mind, whether you’re on the approach to retirement or are decades away yet, it’s crucial to pay attention to your pension.

If you are employed, you likely save into your pension passively each month. While these passive, consistent contributions are a great place to start, you might not have thought about the benefits of being proactive where your pension is concerned.

In fact, MoneyWeek reports that 1 in 5 people does not even know how much is going into their pension each month, and a previous report suggests that nearly 30% of people have “no idea” about their specific retirement needs.

Here’s how to pay greater attention to your pension savings.

Speak to your employer about increasing your contributions (or do this manually if you’re self-employed)

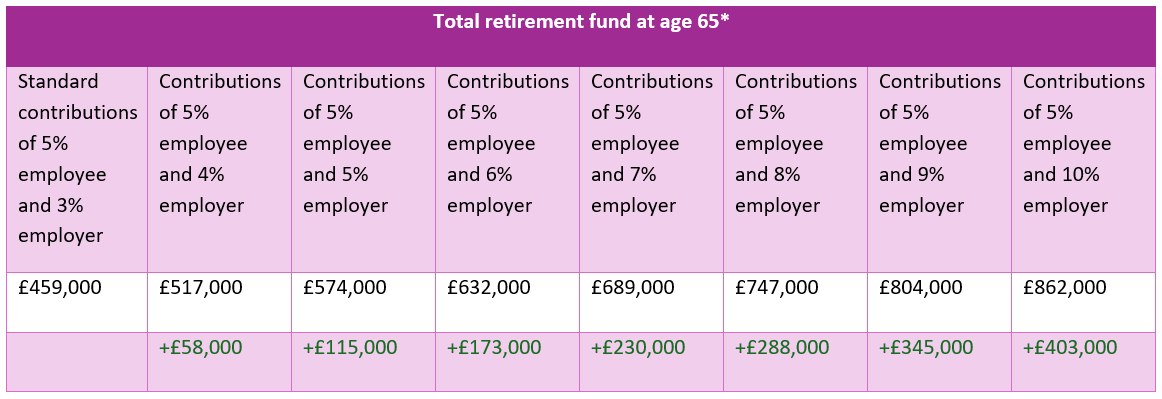

If you’re employed, one of the simplest yet most effective actions you can take today is to speak to your employer about increasing your monthly pension contributions. They might even offer to match or exceed your contributions, adding significant value.

In an example published by Standard Life, you can see that increasing contributions by just 2% could leave you £115,000 better off in retirement.

*Assumes a £25,000 starting salary, 3.50% salary growth a year, and 5% a year investment growth. Figures are not reduced to take effect of inflation. Annual Management Charge of 0.75% assumed. The figures are an illustration and are not guaranteed. Earning limits not applied.

Source: Standard Life

If you’re self-employed, you may be paying into a self-invested personal pension (SIPP) or similar – in which case, increasing your monthly contributions by a small percentage could still make the world of difference later.

It’s never too early or late to make an affordable increase to your contributions, and over time, the returns your pension sees could prove hugely valuable.

Read more: Your retirement choices – how to generate an income later in life

Track down old pension pots and come up with a strategy to improve annual gains

Data published by Standout CV suggests that the days of having one role for your entire career are long gone. In fact, the average Brit will have nine jobs in their lifetime, with this number increasing to 15 for the millennial generation.

After the introduction of automatic enrolment in 2012, most employees will have begun paying into a new pension pot every time they change employers. If you don’t keep track of these pots, you could end up with several small pensions accruing minimal returns, potentially leaving you with less wealth to draw from once you reach retirement.

Indeed, the PLSA says there is an unbelievable £31.1 billion sitting in unclaimed, inactive, or lost UK pensions. If you’re looking to build wealth for retirement, start with the wealth you already have – and this means contacting old employers, getting in touch with providers, and collating the details of all the pensions you hold.

Once you have done so, you can begin to form a strategy for improving gains. This might include consolidating these pensions, but every case is different, so it’s wise to speak with a professional before taking action.

Claim as much tax relief as possible on pension contributions

When you pay into a workplace pension, SIPP, or another type of private pot, tax relief is usually added at source, at the basic rate of 20%. Simply put, the money that would have gone to the government in the form of tax is added to your pension instead, boosting your pot further.

However, many people don’t realise that if you pay higher- or additional-rate Income Tax on a portion of your earnings, you can claim tax relief at your marginal rate.

Unlike basic-rate relief, this won’t be added automatically; you need to complete a self-assessment tax return in order to claim it. If you’ve missed out on higher or additional-rate tax relief in previous years, you can back-date this relief for up to four previous financial years.

Taking this additional step might mean your pension receives a further “free” injection of capital every year between now and when you retire.

Work with a financial planner at Engage Wealth Management

Here at Engage, we are committed to helping individuals like you fund your dream retirement. We can work with you to ensure that your strategy is up to scratch, giving you the confidence to save, invest, and make exciting plans for this next chapter of your life.

Email us at [email protected], or call 01273 076 587.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning or tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.