Making plans is exciting. We love helping our clients to build wealth so they can one day make work optional.

However, even the best-laid plans go wrong.

On a personal and business level, a serious accident, illness, or unexpected death can wreak havoc on families, staff and other shareholders. Thankfully, there are ways to insure against these disasters.

We work with you to build a comprehensive plan to protect your family and, if applicable, your business.

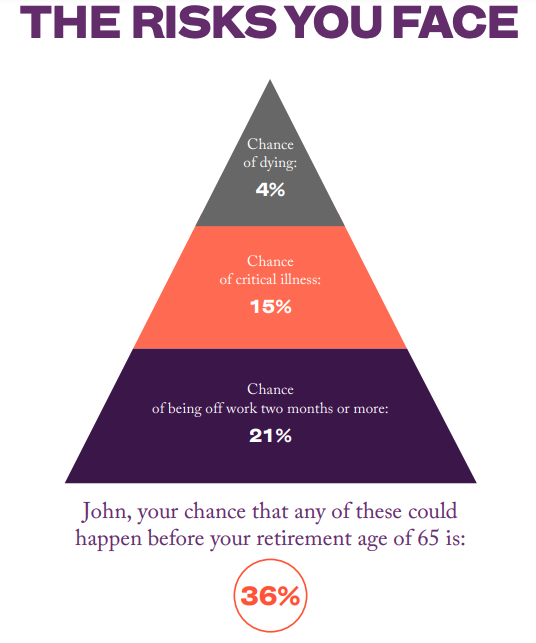

Take a look at the risks faced by a healthy 40-year-old male below:

Source: Royal London risk report - The Institute and Faculty of Actuaries’ Continuous Mortality Investigation insured lives incidence rates. Incidence rates for the entire population may be different to those lives that take out insurance products On a personal level, this can include:

On a personal level, insurance may include the following:

Life Insurance: A lump sum or income paid upon death. For example, to cover a mortgage debt or the cost of raising children.

Critical Illness Cover: A lump sum paid on the diagnosis of a serious illness. Ideal for covering the cost of lifestyle changes, paying off a debt or covering the cost of treatment not available on the NHS.

Income Protection: A regular income designed to cover part of your salary lost due to a serious accident or illness.

For businesses, this might include:

Relevant Life Policy: a cost-effective way for an employer to arrange life cover on an employee’s life, with the benefit payable to the employee’s family or financial dependents. This should be tax efficient for employers and employees as long as it meets specific legislative requirements.

Key Person Insurance: Key person insurance protects businesses against the loss of profits if an employee becomes terminally or critically ill or dies. The money can be used to find a replacement. Key person insurance can help keep the business trading.

Shareholder protection: Shareholder protection allows business owners to repurchase shares from a co-shareholder diagnosed with a critical or terminal illness or dies. This policy helps surviving owners stay in control and minimises disruption to the business.

Smart investors subscribe here

Join 2,000+ readers getting exclusive financial insights every month!