The Bank of England (BoE) raised the base interest rate by another half a point in June 2023. This is its 13th consecutive rise, bringing the bank base rate to 5% – its highest level since April 2008.

Read on to understand why interest rates are on the rise and how the latest increase may affect you and your finances.

1. Rising inflation has prompted the BoE to raise interest rates

The primary reason for yet another rate hike is the persistent inflation the UK has been experiencing since 2021. Although market pundits had hoped that inflation would have reduced substantially by now, it currently stands at 7.9% as of June 2023.

While an inflation rate of 7.9% is significantly reduced from the peak of 11.1% in October 2022, there’s still some distance to go before it reaches the BoE’s official 2% target.

Several combining factors have conspired to create the cost of living crisis, many of which have been repeatedly discussed in news headlines. They include:

- The Covid-19 pandemic

- The war in Ukraine

- Energy prices.

The UK is also experiencing significant labour shortages. In part, this is a result of many people deciding not to return to work after the pandemic ended, taking early retirement, indefinite sick leave, or simply becoming economically inactive.

The problems we need to overcome to bring inflation down to the target rate of 2% are not simple to solve, which is why we’ve seen regular interest rates rise.

Ultimately, higher interest rates typically mean that people tend to spend less on goods and services. In theory, this should help to balance out consumer demand and slow down inflation.

2. High interest rates can have a positive effect on your cash savings

Although banks and building societies have been accused of being slow to pass higher savings rates to customers, the rising rate is starting to filter through to savings accounts.

For example, the best rate on an easy access savings account as of 20 July 2023, according to Moneyfacts, is 4.51%. Meanwhile, if you’re willing to wait 90 days to make a withdrawal, you could earn as much as 5.35% interest.

Although this is welcome news for savers, if you have a lot of cash savings, rising interest rates may mean you’re more likely to have to pay some tax on interest you earn.

Cash savings benefit from a tax-free allowance on interest earned. Your “Personal Savings Allowance” (PSA) is determined by your Income Tax band. In the 2023/24 tax year, the PSA breaks down like this:

- £1,000 for basic-rate taxpayers

- £500 for higher-rate taxpayers

- £0 for additional-rate taxpayers.

Any interest earned that exceeds your PSA may incur a tax charge. So, if you’re a basic-rate taxpayer, you can earn £1,000 in interest before being taxed on any excess.

An alternative option may be to use a Cash ISA. Everyone has an annual ISA allowance (£20,000 in 2023/24), allowing you to make the most of tax-efficient savings.

With interest rates at their highest level in 15 years, you may be tempted to keep more cash than usual on hand. However, with inflation still high, the real-term spending power of money you keep in savings is shrinking.

It’s important to keep an emergency fund on hand to help cover around six months of household spending. If you have additional cash that you don’t expect to need to spend in the next five years, it may be worth considering investing it instead of stashing it in the bank.

3. Increased interest could mean your debt repayments are more expensive

While higher interest rates typically represent good news for savers, according to a report in the Guardian, more than a million mortgage holders could lose up to 20% of their disposable income in the face of rising repayments.

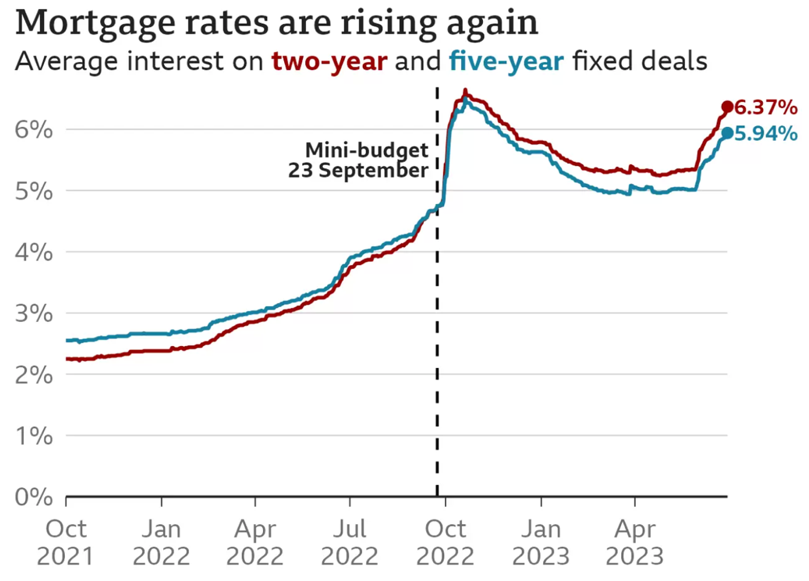

The average rate on a two-year fixed-rate mortgage has increased from 6.3% in May to 6.37%. Meanwhile, the average fixed rate on a five-year deal was 5.91% in May and this has increased to 5.94%. The steep rise is illustrated to great effect in the chart below:

Source: BBC News

Even before the most recent interest rate rise, newspaper headlines had been making much of the increasing costs of mortgage repayments. And, in June 2023, the government succumbed to pressure and stepped in with a package of measures to help support struggling homeowners.

The new mortgage charter provides support for residential mortgage customers, and includes several important commitments, including:

- Customers won’t be forced to have their homes repossessed within 12 months from their first missed payment.

- Customers nearing the end of a fixed-rate deal will be offered the chance to lock in a deal up to six months ahead of their current deal ending. They will also be able to apply for a better deal right up until their new term starts, if one is available.

- A new agreement between lenders, the Financial Conduct Authority (FCA), and the government permits customers to switch to an interest-only mortgage for six months or extend their mortgage term, in order to reduce their monthly payments and switch back to their original term within the first six months if they choose to. Both options can be taken with no need for a new affordability check and won’t affect their credit score.

- Support for customers who are up to date with payments to switch to a new mortgage deal at the end of their existing fixed-rate deal without another affordability check.

While most attention is focused on the rising cost of mortgage repayments, other forms of debt, such as credit cards and car loans, is also likely to have become more expensive.

4. The BoE could continue to raise interest rates if inflation does not fall

Many fund managers and financial experts had expected that the BoE would have resisted further interest rate increases by June 2023. But Schroders report that they expect rates to rise even further – anticipating them to peak at 6.5% by the end of 2023.

Until inflation starts to unstick itself, it’s highly doubtful that the BoE will reduce the bank base rate. As Schroders senior European economist and strategist says, it’s likely that “the Bank will keep hiking until either inflation is close to being at target, or the market is no longer demanding rate rises”.

5. A financial planner can help assess how rising interest may affect you

In a rising interest rate environment, professional advice is invaluable.

Whether you are concerned about the increased pressure on your household finances because of increased mortgage repayments, or are worried about how to meet the persistent higher costs of living in retirement, we can help you understand your options.

If you have any questions about anything you’ve read here or elsewhere in the news, please don’t hesitate to get in touch.

Email us at [email protected], or call 01273 076 587.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

The Financial Conduct Authority does not regulate mortgage advice.