Everyone knows the shocking statistic that 1 in 2 of us will get cancer in our lifetime. Did you also know it’s costs an average of £230,000 to raise a child to age 21?

The chances of you dying prematurely are slim, but if you have anyone depending on you financially then life insurance should be the foundation of any sensible financial plan. A competitive market also means that most people overestimate the price of life insurance.

As financial planners we advise on some complex areas. But what about life insurance? That’s simple right? Pay a monthly premium and if the worst happens, you get a lump sum…so why use a financial adviser?

First up – get a quote online and then get the same quote from an IFA. You’ll normally pay the same price, or a lower monthly premium by going to an independent financial adviser. Plus, you’ll be getting advice and have a professional to bounce questions off.

There is a lot to consider with life insurance and everyone’s circumstances are different. But here are a few tips to get started:

- Don’t go to a bank or a restricted financial adviser

Restricted means advisers can only use one, or a few, insurance companies. It’s highly unlikely you’ll be receiving the most competitive quotes.

- Think about who will be impacted

Who will be impacted financially? You can then begin to build a picture of the life insurance you require, such as covering a mortgage, future living costs of your partner & children or leaving a legacy to someone. But don’t just think about the main earner – if one partner is earning the main living and the other providing childcare – both of these roles are incredibly important and worth insuring.

- How much cover do you need?

For a mortgage it’s straightforward – you need life insurance for the mortgage amount, decreasing each year if you’re on a repayment mortgage and for the term of your mortgage. Beyond this, it gets a little complicated. Some people cover a multiple of their salary, such as 5x but there are other ways of calculating the amount required or the financial impact.

- Don’t rely on your employer

Some employers offer a nice employee benefit called Death In Service. This often pays 2-4 times your salary should you pass away, but would you like your family to receive more? You may leave this employer and this employee benefit is the choice of your employer to offer. By arranging your own cover, you’re in control and the life insurance policy will remain in place if you pay the monthly premiums.

- How much can you afford/how much are you willing to spend?

Think carefully about this – you’re insuring the most important things in your life – you, your partner, your children’s future, and your income. You have the opportunity to make everything financially ok should disaster strike so why wouldn’t you. If you’re taking out a mortgage costing £700 per month, think about adding 10% to cover disaster situations. Or think about how much you spend on coffee, takeaways, eating out, drinks and extract some of that budget.

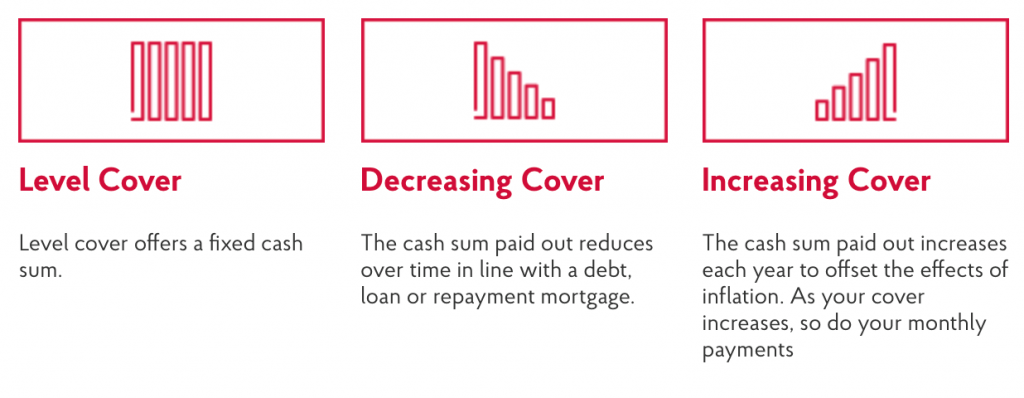

- Level/Decreasing/Increasing

- Consider your health & lifestyle

Your health and lifestyle will impact the level of insurance you can obtain. So, if you’ve had a serious illness, currently smoking or you’re heliskiing every other weekend, expect to pay a little extra or have exclusions applied. I know this from personal experience of a childhood illness, which means I pay double. I’m happy to pay this, as the insurer is taking a risk where they don’t know the long-term effects of my treatment. With a wife and two young children, plus dicing with Sunday morning drivers on my bike every week, it’s an obvious choice for me.

Getting advice is key, as a good financial adviser will work with you to establish what’s important – lets no forget Critical Illness Cover and Income Protection too.

There are other features that could be important, such as joint or single cover, waiver of premium, indexation, placing policies in trust, children’s cover, the insurers reputation & pay-out figures and even the additional support offered such as bereavement & mental health support.

This blog is for information purposes only and should not be relied upon for advice. Always seek regulated advice before proceeding.