If you’re the owner of a limited company, this could be a win-win. Whether you’re a director or looking for life insurance for certain staff then a Relevant Life Policy could be the answer.

- The business/employer pays no National Insurance on contributions

- The business receives corporation tax relief

- Benefits are not taxed as employment income

- No capital gains tax

- No employee National Insurance

- No inheritance Tax

- The benefits don’t count towards pension lifetime allowance

So, let’s expand a little…

If you’re running a limited company, a Relevant Life Policy could be arranged to provide life insurance to directors or employees.

Many companies offer their staff employee benefits such as life insurance. These are normally arranged under a group life insurance policy known as Death in Service.

If you’re a large employer looking for employee benefits, pop over to our friends at Engage Health Group.

However, if you’re a sole director or just have a few staff, you might not be able to obtain a Death In Service policy. That’s where Relevant Life Policies come in.

What is a Relevant Life Policy?

It’s a form of death-in-service benefit that is set up and paid for by the business. The business owns the policy and pays the monthly premiums, but the person insured will be the staff member or director. The person insured will nominate beneficiaries, normally their family, to receive the funds if they die. A trust is arranged at the start to ensure the funds are paid to the beneficiaries.

The business pays no National Insurance on contributions

If the premiums are fully employer funded, they’re not usually treated as a Benefit in Kind. This means neither the employer nor employee pay National Insurance contributions on the premiums.

The business receives corporation tax relief

Assuming the required rules are met, the premiums are an allowance expense for the business. This means no corporation tax to pay.

Benefits are not taxed as employment income

Again, if fully employer funded then no income tax either.

No inheritance Tax

As the policy is arranged under trust from the outset, no Inheritance Tax is due of the benefits. The trustees will arrange for payment to be made to eligible beneficiaries.

How much does it cost?

Life insurance depends on many factors including age, health and lifestyle, and the level of cover you would like. Luckily for you, I’ve just arranged my own cover to provide some perspective. I am:

35 years old

Non-smoker

£500,000 life insurance

Up to age 60

Monthly premium: £23 per month

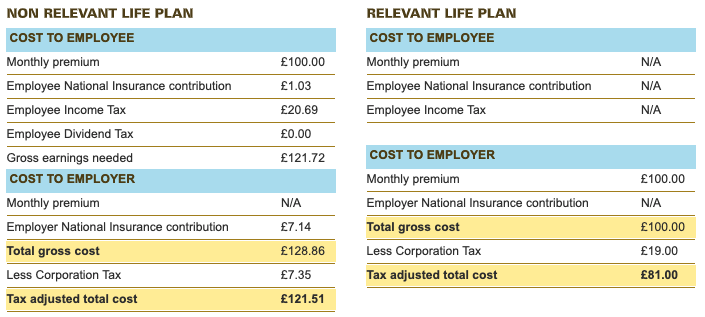

Here is an example of a monthly premium of £100 and the tax benefit of using a Relevant Life Policy:

Take a look at L&G’s RLP calculator.

You might find our previous blog on life insurance useful here.

A Relevant Life Policy can be a great benefit, for directors seeking to arrange or top up their life insurance. Or to provide staff with an employee benefit where a group life insurance policy is not an option. Only life insurance can be arranged in this way, so not Critical Illness Cover or Income Protection.

Don’t forget that business insurance can take many forms such as Relevant Life Policies, Shareholder Protection, Executive Income Protection & Key Person Insurance. It is worth engaging with an expert if you’re reviewing your own needs. At Engage Wealth Management we work with businesses to establish their priorities, your needs and work with you to create a comprehensive protection plan that suits everyone.

To discuss your business insurance needs, whether you’re based in Brighton, Sussex or further afield please give us a call on 01273 076587 or email [email protected]

Why use Engage Wealth Management?

- There is no fee for our advice on insurance

- We are independent, meaning we search the market for the most competitive rates

- We are experts in business insurance and business owners ourselves

- Don’t take our word for it, take a look at VouchedFor to read what our wonderful clients say

*This blog is for information purposes only and should not be relied upon for advice. Always seek regulated advice before proceeding